This story is part of CNBC Make It's Millennial Money series, which profiles people around the world and details how they earn, spend and save their money.

At 26, Victor Yang can still vividly picture the sign his parents hung above his bedroom door growing up: "Time management is the key to success."

The sign was a way of life for the Yang family. The mindset helped his parents, who immigrated from China in their 30s, to push through the hardships they faced building a life in the United States. And they passed the mantra on to Yang, he tells CNBC Make It.

Victor Yang walks around his neighborhood in Washington, D.C.

CNBC Make It

For Yang, that philosophy plays a large part in how he handles the money he earns working as a congressional aide in Washington D.C. "You spend when you need to spend money on something. But when you don't, then step back and think to yourself, Do I really need to make this purchase?" he says.

Victor Yang (far right) and his family.

Source: Victor Yang

Most of the time, Yang answers 'no.' No to hailing an Uber when he can ride his bike. No to eating out when he can cook at home. No to a gym membership when the city provides complimentary facilities. Why would he pay for something when there's a free solution at his fingertips?

"My parents being first-generation immigrants really taught me the importance of making sure you can maximize everything that you are provided," he says.

Earning a living as a public servant: 'It's important to give back to the country that you love'

As a congressional staffer with three years experience, Yang earns $45,000 a year. It's not an easy job, either: He typically works more than 40 hours a week and sometimes ends up staying at the office until 9 or 10 p.m.

But for Yang, it's worthwhile. "I'm a big proponent of public service," he says. "I believe it's important to give back to the country that you love." Additionally, he's passionate about seeing more Asian-American representation in politics and government.

Yang's salary has risen nominally every year that he's been on Capitol Hill, but his pay is largely determined by a number of political factors that don't have anything directly to do with him or the office he works for.

Victor Yang works as a congressional staffer on Capitol Hill.

CNBC Make It

Members of Congress are eligible for an automatic salary increase each year, known as a cost of living adjustment, or COLA. However, a majority vote by Congress can block the pay increase from taking effect, which has been the case for the last 10 years.

This issue trickles down: Because staffers' pay is tied to how much their bosses earn, if members of Congress aren't paid more, they aren't able to give their staff more.

It's a hotly contested issue in D.C. Those who oppose the adjustments argue that members of Congress need to earn salary increases, instead of getting them automatically. "Gridlock on major issues must not be rewarded. Members of Congress need a reality check, not a raise," Brian Fitzpatrick (R-Pa.) said in a statement in June 2019.

However, those in favor of the adjustments argue that they are crucial to making it possible for people who aren't independently wealthy able to work for Congress. "We don't want to have only rich people here," House Majority Leader Steny Hoyer (D-Md.) said in June.

While Yang can cover all of his expenses — and is lucky to be able to count on his savings and support from his family in a pinch — he recognizes that not everyone is so fortunate, and that $45,000 a year doesn't cut it for many others who earn a similar salary.

"The low staffer salaries makes it harder for people from disadvantaged or low-income backgrounds to get a job with a member of Congress," Yang says. This disconnect can limit the pool of candidates who are able to accept work on Capitol Hill and reflects a growing unease around pay in Washington.

How Yang budgets: 'My default is saving'

Yang's budgeting philosophy is simple: Spend as little as possible. In any given month, his goal is to keep his expenses below $2,500 and put as much as he can into savings. "I don't budget heavily, I just try to make sure that my expenses don't go over a certain level," he says.

Saving is easier on his salary in part because he graduated from Syracuse University nearly debt-free, thanks to generous financial aid. He only owed about $10,000 in student loans and has already paid it off with support from his parents and tuition reimbursement from his job. He was able to stay on his parents' health insurance plan until he turned 26. And as a federal employee, his metro fare to and from work is completely covered by the government through a program called TRANserve.

Victor Yang commutes to and from work on the D.C. Metro.

CNBC Make It

But Yang is also a savvy budgeter. In college, he worked as a resident advisor for two years in order to earn free room and board. He participated in Sprint's BYOD deal, which got him a free year of service — he only has to pay taxes. Instead of shelling out for a gym membership, Yang takes advantage of the free fitness facilities available to D.C. residents. He also bikes everywhere he can, which is both free and environmentally friendly.

Yang applies the same philosophy to his social life. He looks for cost-effective ways to enjoy himself and spend time with his friends, such as playing basketball at the recreation center near his home.

"My default is saving," Yang says. "I don't spend unless I need to spend."

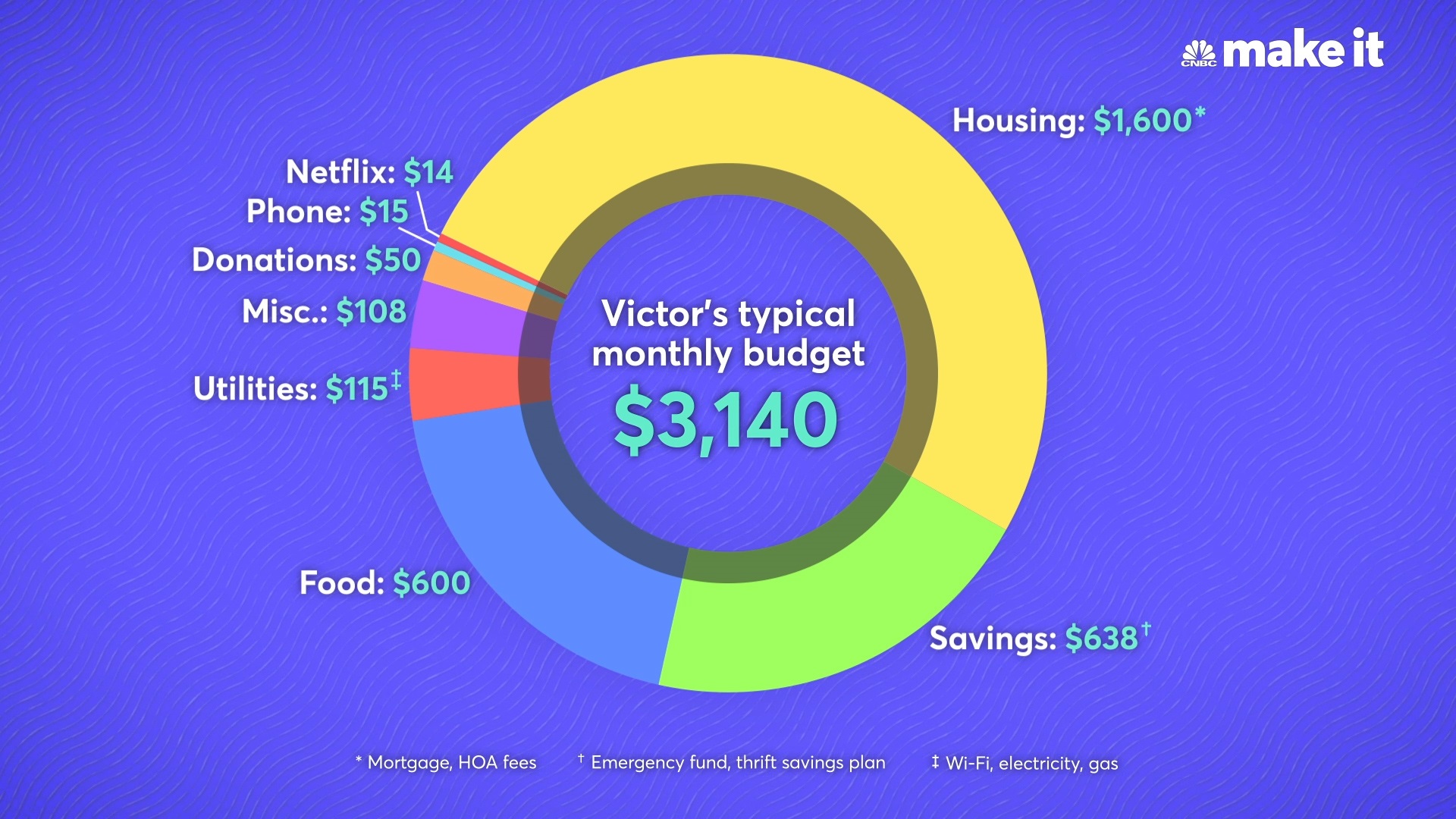

Here's a closer look at how he budgets his income. These numbers reflect Yang's spending activity as of September 2019, when he was still 25 and not paying for health insurance.

Housing: $1,600

Yang owns a two-bedroom, one-bathroom apartment in D.C.'s northeastern quadrant. He pays $1,425 per month on his mortgage and another $175 in HOA fees. He likes living alone, but says he would consider getting a roommate or setting up an Airbnb account if he ever wanted to cut costs even more.

Yang bought the home in 2018 for around $350,000. While his parents covered the down payment, he pays all of the remaining expenses himself.

"[My parents] felt it was important to be financially stable," he says of their decision to help him buy an apartment. "Because they are first-generation immigrants, they really struggled with homeownership and to find stability in a new country."

Owning his apartment also ensures that Yang's housing costs won't rise. "A lot of times people of color and immigrants are priced out of their communities," he says. "We see that happening in Boston's Chinatown, where I'm originally from, and in some of D.C.'s neighborhoods. When you own your home, you're insulating yourself from that."

[My parents] felt it was important to be financially stable. Because they are first-generation immigrants, they really struggled with homeownership and to find stability in a new country.

Choosing where in the city to buy was easy for Yang. Before owning, he rented a place with a friend in the neighborhood and fell in love with the location: "There were basketball courts that were accessible, the recreation center was down the street, there was a library, the grocery stores were nearby. It was perfect for me to access everything that I needed."

"This is an up-and-coming area," Yang says. He's confident that it's not a matter of if the neighborhood will become a hot spot to live, but when.

Savings: $638

Each month, Yang aims to save between $400 and $500, but the exact amount varies depending on his expenses for the month. During busy periods at work, he might attend several receptions and events in a week and not spend as much on food or social activities.

Victor Yang graduating from Syracuse University in Syracuse, New York.

Source: Victor Yang

Yang also has 5% of his paycheck deducted pre-tax and added to his Thrift Savings Plan, which is similar to a 401(k) for government employees. His employer then matches that 5%.

Although Yang doesn't make regular contributions to his Roth IRA, he adds lump sums when he can. In 2018, he contributed his entire annual bonus, which helped him max out the account for the year.

Food: $600

Yang spends about $500 a month on groceries and another $100 (or less) dining out. He loves to cook and tries to eat at home as much as possible. Typically, he brings lunch to work.

Yang is willing to splurge on pricier grocery items from time to time. "I really like seafood, so I spend money on seafood, which is expensive," he says. "Chicken is cheaper."

One small perk of his job is that he attends numerous catered events each month. If he ends up eating dinner at an event, it saves him on grocery costs for the week.

Miscellaneous: $108

Yang has three credit cards, but primarily uses one that earns him travel rewards. It's the only one of the three with an annual fee and costs him $100 a year, or about $8 per month.

He also spends around $100 on miscellaneous expenses each month, which can range from dish soap and toothpaste to going to the movies with friends. He isn't strict about what he spends on, as long as it's not too much. Occasionally, he'll splurge on a new game for his Xbox One.

Victor Yang in Washington, D.C.

CNBC Make It

Yang absolutely refuses to spend money on coffee. "It's a complete waste," he says. "The coffee costs 5 cents to make and someone's selling it for $2." Another reason to avoid buying lattes: "Graham Stephan says so," he jokes.

Everything else:

- Utilities: $115 (includes Wi-Fi, electricity and gas)

- Donations: $50

- Phone: $15

- Netflix: $14

What experts say: 'It's pretty impressive to see this level of organization'

CNBC Make It asked Douglas Boneparth, certified financial planner and president and founder of Bone Fide Wealth, to comment on what Yang is doing well and where he could improve.

Douglas Boneparth, certified financial planner and president and founder of Bone Fide Wealth.

Source: Douglas Boneparth

Yang is organized and disciplined with money

Overall, Yang is doing an excellent job with his finances, Boneparth says. "It's pretty impressive to see this level of organization from someone this young."

Yang knows exactly where his money goes each month and aims to keep his expenses under a certain amount so that he's able to consistently save. As Boneparth puts it, he has an "intimate understanding of how money comes into and out of his life. It's almost as if every penny is accounted for."

Victor Yang rides his bike everywhere he can. It's both cost-effective and eco-friendly.

CNBC Make It

Mastering your cash flow, like Yang has, is crucial to financial health. Not only does it allow you to understand how much money you're bringing in, but also how much you have left after expenses to contribute to other goals, such as saving for retirement.

It's smart to think about what's next

In terms of handling money well, Yang has already checked off several boxes: He's mastered his cash flow, he has emergency savings and he's investing for the future. But now he should ask himself, What's my next big goal?

Identify your goals early and quantify them. When do you want to achieve the goal? And how much is it going to cost? Once you have the basic mathematics, you can make an informed decision.

Douglas Boneparth

president and founder, Bone Fide Wealth

"Identify your goals early and quantify them," Boneparth says. "When do you want to achieve the goal? And how much is it going to cost? Once you have the basic mathematics, you can make an informed decision."

It's worth noting that Yang's current habits and future goals might not be the same as others who earn a similar salary, Boneparth says. That's OK: "Everyone should view their situation independently of anyone else's."

Yang chooses to live frugally, and it's working for him. But it's not the only smart way to manage money. "The hardest part of personal finance is striking a balance between your subjective lifestyle and saving toward your goals," Boneparth says.

He has the potential to earn more

If Yang wants to increase his income, he's in a good place to think about how to do it in a way that aligns with his lifestyle. "Not that he has to, but how does he get from $45,000 to $90,000?" Boneparth asks. "Is that through further educating yourself and making an investment in education? Is that through a promotion or what's next in his career? Or is that through entrepreneurial spirits and a side hustle?"

It's smart for Yang to keep in mind that cutting back isn't the only way to control the amount he's able to save, Boneparth says.

Victor Yang texts while riding the D.C. Metro.

CNBC Make It

But overall, earning a big salary isn't a driving force for Yang. "I think that money is a tool in life," he says. "It's really important, but it's not something that should be idolized or glorified. I would like to make more money, but it's not something that I am completely hellbent on."

What's your budget breakdown? Share your story with us at makeitcasting@nbcuni.com for a chance to be featured in a future installment. We are especially interested in hearing from people in Austin, Denver and Nashville.

Like this story? Subscribe to CNBC Make It on YouTube!

Don't miss: How a 28-year-old homeowner making $80,000 a year in DC spends her money

"earn" - Google News

December 05, 2019 at 11:54PM

https://ift.tt/34TXKRc

How a 26-year-old congressional aide earning $45,000 spends his money in Washington, DC - CNBC

"earn" - Google News

https://ift.tt/2YgSjJr

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Bagikan Berita Ini

0 Response to "How a 26-year-old congressional aide earning $45,000 spends his money in Washington, DC - CNBC"

Post a Comment